Summer STR Pacing Update: Demand Holding Strong Amid Economic and Geopolitical Uncertainty

Quinn Monescalchi

6/1/2026

Sponsored by Key Data Dashboard

As of May 12, summer pacing across many major short-term rental markets is showing a more nuanced story than simple top-line booking growth. The broader travel environment entering summer 2026 is being shaped not only by evolving consumer spending behavior but also by continued geopolitical and economic uncertainty.

Ongoing conflicts in Eastern Europe and the Middle East, continued trade tensions between major global economies, elevated interest rates, and renewed volatility in equity markets have all contributed to a more cautious consumer backdrop compared to the aggressive post-pandemic travel surge seen in recent years.

At the same time, U.S. inflation has moderated compared to peak levels seen in 2022 and 2023, though gasoline prices have moved higher again heading into the peak summer driving season. Rising fuel costs may place additional pressure on discretionary travel budgets, particularly for drive-to leisure travelers and larger family groups, potentially contributing to shorter booking windows and greater price sensitivity in some vacation markets.

A Summer Market Increasingly Driven by Pricing Power

Despite these broader macroeconomic pressures, the short-term rental industry continues to show resilience across many popular summer destinations. However, the composition of that growth has changed meaningfully. Rather than relying primarily on occupancy expansion, many markets are now being supported by pricing power, with ADR growth continuing to drive RevPAR gains even as booking pace normalizes in several destinations. Booking windows also continue to compress in many regions, while average stay lengths appear to be stabilizing after several years of post-pandemic volatility. While several destinations are seeing softer occupancy growth or slower booking velocity compared to last year, revenue trends remain surprisingly resilient thanks to continued ADR expansion across many leisure markets. The result is a summer outlook that appears more rate-driven than volume-driven in many destinations.

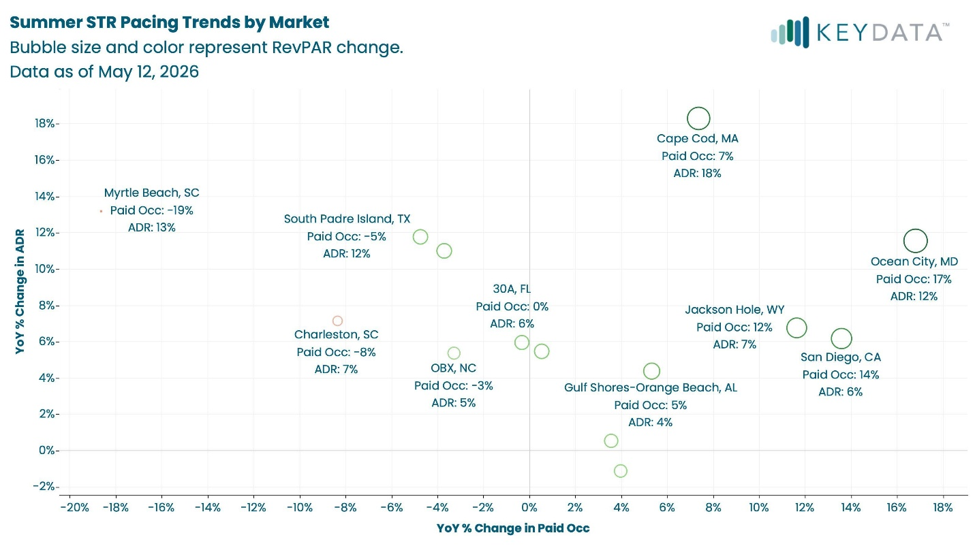

To better illustrate how summer pacing trends are evolving across major short-term rental markets, the accompanying scatterplot maps each destination by year-over-year changes in paid occupancy and ADR as of May 12, 2026. Markets positioned farther to the right are seeing stronger occupancy growth relative to last year, while markets higher on the chart are experiencing stronger ADR growth. Bubble size and color both represent year-over-year RevPAR change, allowing the strongest overall performers to stand out visually.

The upper-right quadrant represents markets where both occupancy and pricing are increasing year over year, signaling some of the strongest overall summer pacing conditions. Markets such as Cape Cod, Massachusetts; Ocean City, Maryland; Jackson Hole, Wyoming; and San Diego, California; fall into this category, reflecting healthy traveler demand alongside continued pricing power. The upper-left quadrant highlights destinations where ADR growth is outpacing occupancy trends, indicating operators are still pushing rates higher despite softer booking demand. Myrtle Beach, South Carolina; South Padre Island, Texas; and Charleston, South Carolina; are examples of markets currently experiencing this dynamic.

Meanwhile, the lower-right quadrant represents markets where occupancy growth is outpacing ADR performance, suggesting demand remains healthy even as pricing growth moderates. The Hawaiian Islands fall into this category, reflecting stable summer travel demand alongside softer ADR gains compared to several mainland resort markets.

Collectively, the visualization reinforces one of the clearest themes emerging this summer: In many destinations, RevPAR growth is increasingly being driven by pricing strategy rather than substantial occupancy expansion.

Markets Showing Strong Momentum

Beach markets continue to show some of the strongest pricing power heading into the summer season. Cape Cod stands out as one of the strongest performers year over year. ADR growth of 18.3% has helped drive RevPAR growth of 17.2% year over year, while paid occupancy has also improved 7.4% compared to last summer. The market continues to benefit from strong seasonal demand and relatively stable stay length trends heading into peak summer travel. The market’s gains are being driven primarily by ADR growth, which has allowed revenue per available rental and revenue per property to accelerate meaningfully. Occupancy metrics are also improving, suggesting travelers remain willing to pay premium rates for highly seasonal coastal inventory.

The Gulf Shores and Orange Beach, Alabama, market is also entering the summer in a healthy position. ADRs are up 4.4% year over year, while RevPAR growth is approaching 10%, indicating operators are successfully balancing occupancy gains with continued pricing strength. Booking windows in the market remain relatively healthy for a drive-to destination, although some operators are reporting more last-minute booking behavior compared to prior summers. While inventory growth has slowed slightly year over year, booked nights, occupancy, and revenue metrics are all pacing ahead of last year. Revenue growth is notably outpacing occupancy growth, reinforcing the broader trend that pricing continues to be the primary driver of top-line gains. The market appears to be benefiting from sustained regional drive-to demand and relatively strong booking consistency.

Jackson Hole is pacing as one of the strongest luxury-oriented mountain destinations for the summer season. The market is seeing double-digit paid occupancy growth alongside continued ADR expansion, helping drive substantial RevPAR acceleration year over year. Longer average stay lengths in luxury mountain markets continue to provide stability for operators despite broader economic uncertainty. The market is seeing double-digit growth in booked nights and occupancy, while ADR growth is adding another layer of momentum to overall revenue performance. Revenue per available rental is pacing substantially ahead of last year, signaling continued demand for high-end experiential travel despite broader concerns around consumer softness.

Hawaii is showing a steadier but still positive summer outlook. Paid occupancy is pacing modestly ahead of last year, while RevPAR trends remain positive despite softer ADR growth compared to several mainland resort markets. Booking windows remain shorter than historical norms, reflecting broader consumer caution around travel spending. The islands are pacing ahead of last year across most demand and revenue indicators, although growth is more moderate compared to some mainland leisure markets. ADR performance has softened slightly year over year, but occupancy and booked nights are both improving, allowing overall revenue growth to remain positive. This suggests Hawaii is continuing to recover demand while relying less heavily on aggressive rate increases than some domestic resort markets.

When Pricing Outpaces Demand

Several markets, however, are showing signs of softer booking momentum despite healthy pricing conditions. Charleston is one of the clearest examples. Paid occupancy has fallen 8.4% year over year in Charleston, though ADRs are still up 7.1%. As a result, RevPAR declines have remained relatively modest despite noticeably softer booking momentum. The market may be experiencing increased traveler price sensitivity as guests continue weighing higher accommodation costs against broader economic pressures. ADRs are up meaningfully year over year, but booked nights and occupancy are pacing below last summer. Revenue growth has softened as a result, with the market appearing to trade stronger pricing for lower conversion volume. This may indicate growing price sensitivity among travelers or increased competition from alternative regional destinations.

Myrtle Beach is experiencing some of the sharpest demand softness among the larger summer leisure markets in the dataset. Paid occupancy is trailing last year meaningfully, even as operators continue pushing ADRs higher. The market reflects a growing divide between pricing ambitions and consumer willingness to absorb higher vacation costs in more value-oriented beach destinations. Shorter booking windows may also be contributing to softer pacing visibility in the market. While ADRs have increased considerably year over year, occupancy and booked nights are pacing notably below last year’s levels. The market’s revenue trends have slipped slightly negative, as higher pricing has not been enough to offset weaker booking activity. This could suggest that value-oriented travelers are becoming more selective heading into peak summer.

The north Georgia mountains market is telling a similar story on a smaller scale. Softer paid occupancy trends have limited overall growth, though operators have managed to offset some of the slowdown through moderate ADR gains. RevPAR growth remains relatively flat year over year, highlighting the challenge many secondary drive-to mountain markets face after several years of outsized pandemic-era demand.

Ocean City is emerging as an interesting outlier among beach destinations. The market is pacing ahead across paid occupancy, ADR, and RevPAR metrics, with particularly strong RevPAR growth indicating healthy summer demand and continued traveler willingness to absorb higher nightly rates heading into peak season.

Booking Behavior Continues to Normalize

Urban-adjacent leisure markets are also beginning to show more normalization compared to the outsized growth rates seen over the last several years. Consumers appear to be booking closer to stay dates in many regions, creating a pacing environment that feels softer on the surface despite relatively stable underlying travel demand. This shorter booking window dynamic has become increasingly common throughout 2025 and into 2026, particularly as travelers remain cautious about discretionary spending decisions amid continued economic uncertainty.

Luxury Travel Holds Strong While Value Segments Face Pressure

Another notable trend this summer is the continued divergence between high-end and value-oriented travel segments. Luxury and experiential destinations are generally maintaining stronger pacing trends, with travelers in higher income brackets appearing less sensitive to rising nightly rates and broader economic pressures. This has allowed several premium leisure destinations to continue posting strong ADR and RevPAR growth heading into the summer season. Meanwhile, more price-sensitive drive-to and family-focused vacation markets are beginning to show signs of demand resistance as consumers balance travel spending against broader household expenses.

Air Travel and Global Dynamics Shape Regional Performance

Air travel trends may also be influencing regional performance disparities. While international travel demand has continued recovering globally, higher airfare volatility and shifting international exchange rates may be contributing to stronger domestic demand in certain U.S. resort and drive-to markets.

At the same time, some international gateway destinations appear to be experiencing softer pacing relative to prior years as travelers weigh broader economic and geopolitical conditions when planning longer-haul vacations.

The Summer Story Is Revenue Optimization

Across the broader dataset, one of the clearest themes is that ADR growth continues to outpace paid occupancy growth in many major summer destinations. Several markets are successfully generating RevPAR gains despite softer occupancy trends, underscoring how professional operators are increasingly prioritizing yield management and pricing optimization over pure occupancy maximization. At the same time, compressed booking windows and stabilizing stay lengths continue shaping pacing dynamics across both drive-to and fly-to leisure destinations.

Overall, the broader summer pacing story for 2026 is less about explosive occupancy growth and more about revenue optimization. Across many markets, operators are still successfully pushing rates higher even as booking growth normalizes or softens. Markets with strong experiential demand and limited high-quality supply continue to outperform, while more price-sensitive destinations are beginning to see resistance to continued ADR expansion. As the industry moves closer to peak summer travel dates, the key question will be whether late-season demand materializes strongly enough to support current pricing strategies or whether operators will need to become more aggressive with discounts to sustain occupancy momentum.

Quinn Monescalchi

Quinn Monescalchi is a senior data analyst for marketing and insights with Key Data Dashboard.